It was after the birth of her second child in the late 1990s that Marguerita Cheng broached the first of many conversations with her parents about their finances. With her family expanding, Cheng used this life event to encourage her parents to start thinking (and talking) about their plans for the future.

Cheng’s mother, who was in her mid-50s at the time, responded: “Why are we talking about stuff for old people?” Cheng’s father, then in his late 60s, was more immediately receptive to talking about things like estate planning and long-term care—and her mother soon got onboard, as well. “They realized that by planning, they were doing it as a gesture and a symbol of love,” Cheng says.

Within a few years, these conversations became prescient when Cheng’s father was diagnosed with Parkinson’s disease. And while the final three years leading up to her father’s death in 2015 were “really hard,” Cheng says, having a plan in-place years before the family needed around-the-clock care for her father helped to reduce one potential source of stress at a time when family members were already struggling emotionally. “My dad would say: ‘Just because you don’t talk about these things doesn’t mean they’re not going to happen, and just because you do doesn’t mean you’re jinxing yourself.’”

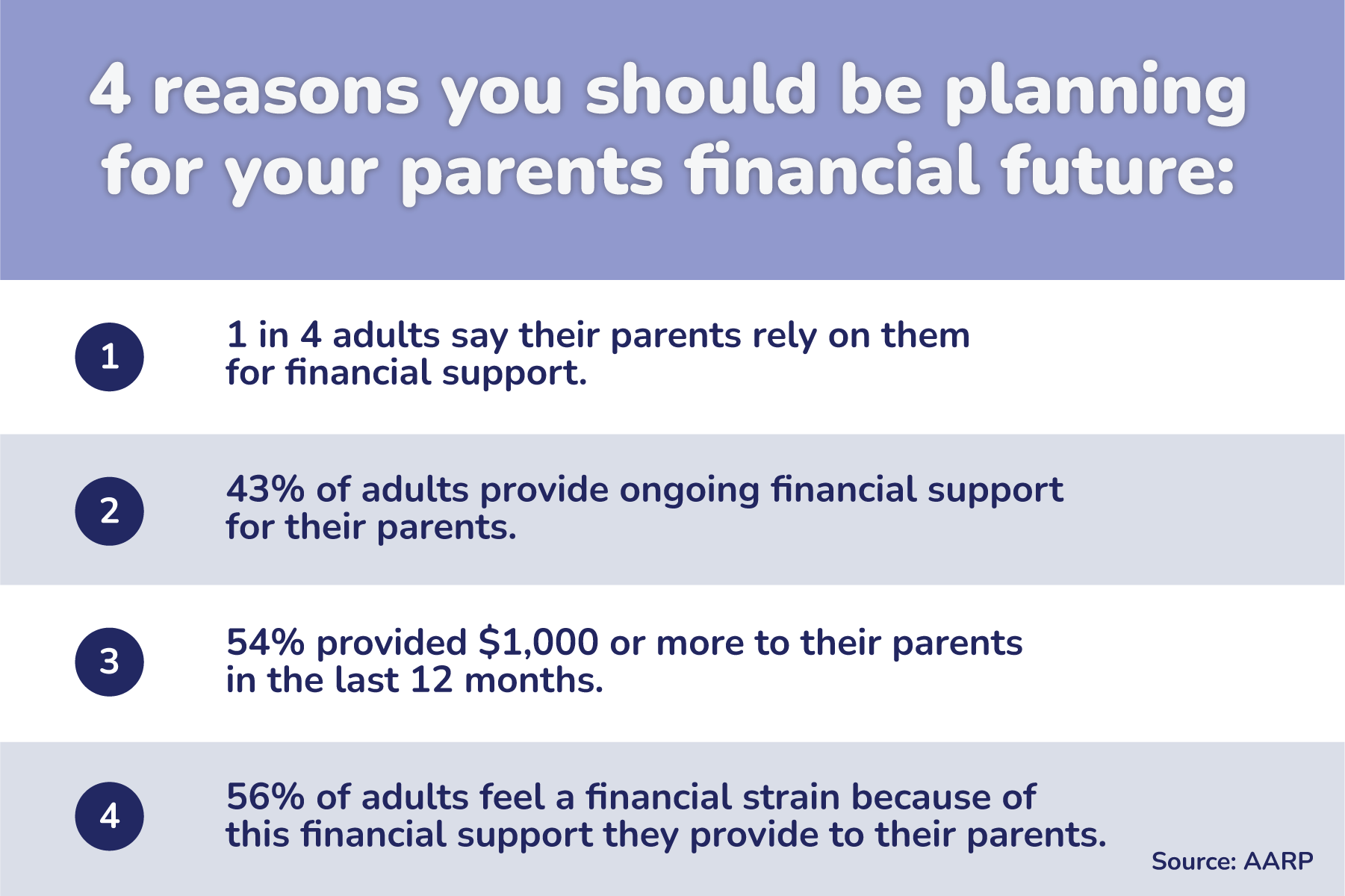

In addition to her expanding family, Cheng was motivated to talk with her parents about their finances because she had started thinking about a simple question: How would she divide $100 between her nuclear family and her parents, in the event they needed her financial help? That’s a reality many Americans grapple with: A 2019 survey by AARP found that 32% of adults ages 40 to 64 had provided regular financial support to their parents in the past year and 42% said they expected to do so in the future.

Although Cheng’s parents didn’t ultimately need her financial help, she sees this dynamic in her day-to-day role as a certified financial planner and the founder and CEO of Blue Ocean Global Wealth. Many of her clients, particularly those in the Gen X generation, are currently “in the thick of it,” between caring for kids and helping with aging parents, Cheng uses her experience to urge others to broach the money conversation with parents as early as possible.

“Talking with your aging parents can be really difficult,” she says. “But the sooner you start, the longer window you have.”

Talking about money can be as natural as talking about the weather in some families, while the topic can be awkward and even contentious in others. Here’s how to navigate these all-important talks with your parents, and what you should plan to cover.

Spend time strategizing first

When it comes to conversations of substance, even cheerful ones like offering a new hire a job or proposing to your future spouse, you probably think through the talk first and don’t just ‘wing it.’ The same goes for talking with your parents about their finances and plans for the future.

By the way, if you feel like you’re behind-the-ball, you’re not: 73% of Americans haven’t had extensive conversations about finances with their aging parents, according to a 2017 survey conducted by GoBankingRates. Fear largely explains why, as respondents reported their top reasons for not broaching this topic were: they didn’t know how to start the conversation, and they were afraid their parents will either think they’re being nosy or motivated by money.

Whether it’s because they don’t want to face their own mortality or discuss the ins-and-outs of their finances or they fear the children will fight over finances after they’re dead, sometimes parents aren’t so keen to have the conversation, either. The GoBankingRates survey found that 23% of children had tried to bring up the subject of finances, but their parents refused to discuss the topic.

It’s important to start off on the right foot, so you should spend time thinking about why your parents may be reluctant to have these conversations so you can avoid touching on any sources of embarrassment or other sore spots, recommends Cameron Huddleston, author of the book, Mom and Dad, We Need to Talk: How to Have Essential Conversations With Your Parents About Their Finances. Involving your siblings is crucial because if you bypass them to dive straight into the specifics of your parents’ finances, that could create anger, resentment and even suspicions among your siblings that you are in fact motivated by money, she adds.

“Get on the same page with them,” Huddleston says. Share ideas among your siblings about how to approach your parents, discuss what topics you want to talk about, decide who will lead the conversation, when it will happen, the role each sibling will play in your parents’ lives as they age and even how involved everyone wants to be, she adds.

This type of pre-talk strategizing can go a long way in ensuring a successful first conversation. “How to broach the topic is one of the hardest pieces,” says Aaron Clarke, a certified financial planner and owner of Gig Wealthy. “With family dynamics, there are a thousand different ways it can go.”

Clarke is currently in the process of helping both his parents and other older family members with their financial plans, and that experience has taught the value of asking “really intentional” questions. Otherwise, a poorly worded question could set off emotional triggers that result in the room going quiet, arms getting crossed, and someone saying: “I can’t deal with this right now.” If that type of interaction causes the conversation to shut down, it’s potentially harder to bring up again later, he adds.

Open the door with one conversation

You can’t strategize forever, and eventually need to take the plunge. “No matter how uncomfortable the conversations may be, the time to have them is now,” urges Darin Shebesta, a certified financial planner and vice president of Jackson Roskelley Wealth Advisors. An only child, he finally broke through with his mom about 10 years ago when she was in her early 60s—and she ultimately hired him as her financial planner.

Years earlier, Shebesta had tried to ease into the topic, to no avail. With time, he became more vocal about his concerns for his mother’s future and had also grown his expertise in financial planning—and finally, he was able to break the conversational ice. “It opened up something,” he says. “She didn’t want me to be concerned about her.”

When Shebesta’s mother suffered a stroke a couple years ago, these conversations proved invaluable. “I couldn’t have acted on her behalf if I didn’t have everything in place,” he says. And now he has “zero” financial concerns about her needs for long-term care in the future. “I can focus on being her son rather than her caregiver.”

Because Shebesta’s mother had always been “pretty tight-lipped” about her finances, he centered the conversations around his love for her and concern for her future rather than money—and this is an approach he recommends to others. It’s also okay to admit your fears, he says. “You can say something like: ‘I’ve got an important conversation I want to have with you and I’m concerned about how you’re going to take it.’”

If you do approach your parents with your siblings, as a united force, be sure you don’t make them feel as if you’re ganging up on them, Huddleston says. As with Shebesta, Huddleston says messaging is important, and recommends that you try to communicate the following:

“We care about you, we love you, we want to be able to help you and we want to know what sort of help you might need.”

An open-ended question can also be very powerful, according to Clarke, who says this psychology concept has been helpful in getting reluctant members of his family to open up and has also worked for his clients. He recommends framing questions around prompts like: “Are you open to…” or “Are you interested in knowing what happens…”

Finally, you may need to ease into money conversations if this isn’t a topic your family has readily discussed in the past, Huddleston says. Start by bringing up things that are topical—say, the current bout of high inflation or your own estate planning—before diving into conversations that are more personal, like how your parents’ retirement is going or what they have planned for the future, she adds. “Those first conversations might not even reveal a lot of information about their finances, they might just be opening the door to more conversations.”

The most important documents for your parents to have

Be it your first conversation or your fiftieth conversation with your parents, at some point you do need to get into specifics. While your parents may have plans for the future, what’s key is whether these plans are supported by legal documents that ensure their plans are executed according to their wishes.

“At the very least, you need to find out: Do your parents have basic estate planning documents like a will or a trust?” Huddleston asks. These documents will dictate who gets what when they die to prevent the state where they live from making those decisions, she says. A 2021 Gallup poll found that 76% of Americans ages 65 and up reported having a will that describes how they’d like their money and estate to be handled after their death.

A will is one of the legal documents that is most important for your parents to have:

Will and/or trust—While there can be a lot of overlap in these documents, a will directs how money should be distributed only after the parent who originated the will dies (it’s not recommended for married couples to have a joint will) whereas a trust handles the transfer and management of those assets at any indicated time, during the life or after the death of the creator. It takes effect immediately upon signing it.

Power of attorney—Another legal document, this grants the temporary or permanent authority for someone else to act on your parents behalf when making financial and legal decisions, and while one or both parents are still alive. A power of attorney document may focus specifically on financial or health care decisions—or may be all-encompassing.

Offering to take some burdens off your parents’ plate can be one way to facilitate broader discussions about money, Clarke recommends. “Sometimes the easiest way into this conversation is the power of attorney.”

Becoming your parent’s power of attorney can also be an opportunity for you to serve as a second set of eyes on their finances, Huddleston says. While some parents get a little bit nervous about signing over this authority, they can maintain some control by working with an attorney to draft a document that meets their specifications and also complies with state law, she adds.

Huddleston learned the value of a power of attorney document firsthand while caring for her mother, who was diagnosed with Alzheimer’s disease. In the absence of such a legal document, you may have to go through an arduous court process to be named the conservator of your parent’s estate to manage their finances if they become incapacitated and don’t have a power of attorney, she adds. “It’s absolutely horrible.”

Finally, as important as it is to know if these documents exist—and to help your parents get them set up, if they haven’t already—it’s as important to know where they are located, Huddleston says. “Be sure to ask: ‘Could you tell me where these documents are in case of an emergency?”

Keep the conversation going

When talking with your parents about their finances, the focus isn’t so much about how much money is at stake as it is about their plans for the future and whether they’ll need any help. “These conversations are even more important if your parents don’t have a lot of money because they’re more likely to rely on you for support as they age,” Huddleston says.

For example, Huddleston cites statistics that more than half of American adults over the age of 65 will need long-term care at some point. And yet, “an overwhelming” number of people don’t have a plan for how to pay for it, assuming that it will be covered by Medicare, she adds. “That means they could be relying on you to be a caregiver.”

And when children help out financially, they do so in a pretty big way. That AARP survey found that 54% of Americans had given more than $1,000 to a parent in the last 12 months, while 20% had provided more than $5,000 in assistance.

Even if you don’t have to help your parents financially, Cheng says she learned firsthand just how much of a toll caring for aging parents can be in other ways. “It really affects three generations,” she says, adding that she learned the importance of self-care while caring for her father and raising three young children at the same time.

It’s important to get a sense of your parents’ financial picture when everyone is healthy and can still make changes, if necessary. Find out what types of life and health insurance policies they have, how they pay their bills each month, what investments they have, whether they plan to stay in their current home or move, if they have a plan for drawing on Social Security and other retirement benefits, whether they’ve been working with a financial planner, and what their plans are for long-term medical care. Also check if they have a living will, also known as an advance health care directive, which spells out their wishes for end-of-life medical treatment.

“The more details you can get, the better,” Huddleston says, adding that it can also be helpful to prepare a checklist for your parents to reference.

However, your parents must also be willing to take action. After years of prodding, Shebesta finally began working with his mother and learned that she hadn’t done any estate planning. His first priority was to set up a meeting with his mother and an estate attorney—and within about 6 months, she had her plan in-place. By comparison, conversations in Clarke’s family about his grandparents’ situation have been going on for more than five years. “Getting them to take action is the hardest part,” he adds.

It can be a little tricky to figure out the right cadence that balances being sensitive to your parents while encouraging them to take action. “You don’t want to be having these conversations every time you talk to your parents,” Huddleston says, adding that making “money dates” can be a way to keep the dialogue going. What’s more, Huddleston has received a lot of feedback on her book from parents who are more willing than the children to broach uncomfortable topics, which is why she’s thinking about writing a follow-up book to help older adults talk about their finances with their adult children..

Similarly, Clarke says that his experience with his family has taught him how important it is to get financial conversations started early—which is why he broaches these topics with clients even when they’re only in their 30s.

“Don’t forget to do this for yourself and for your children,” he says. “There’s no reason you can’t do both at the same time.”